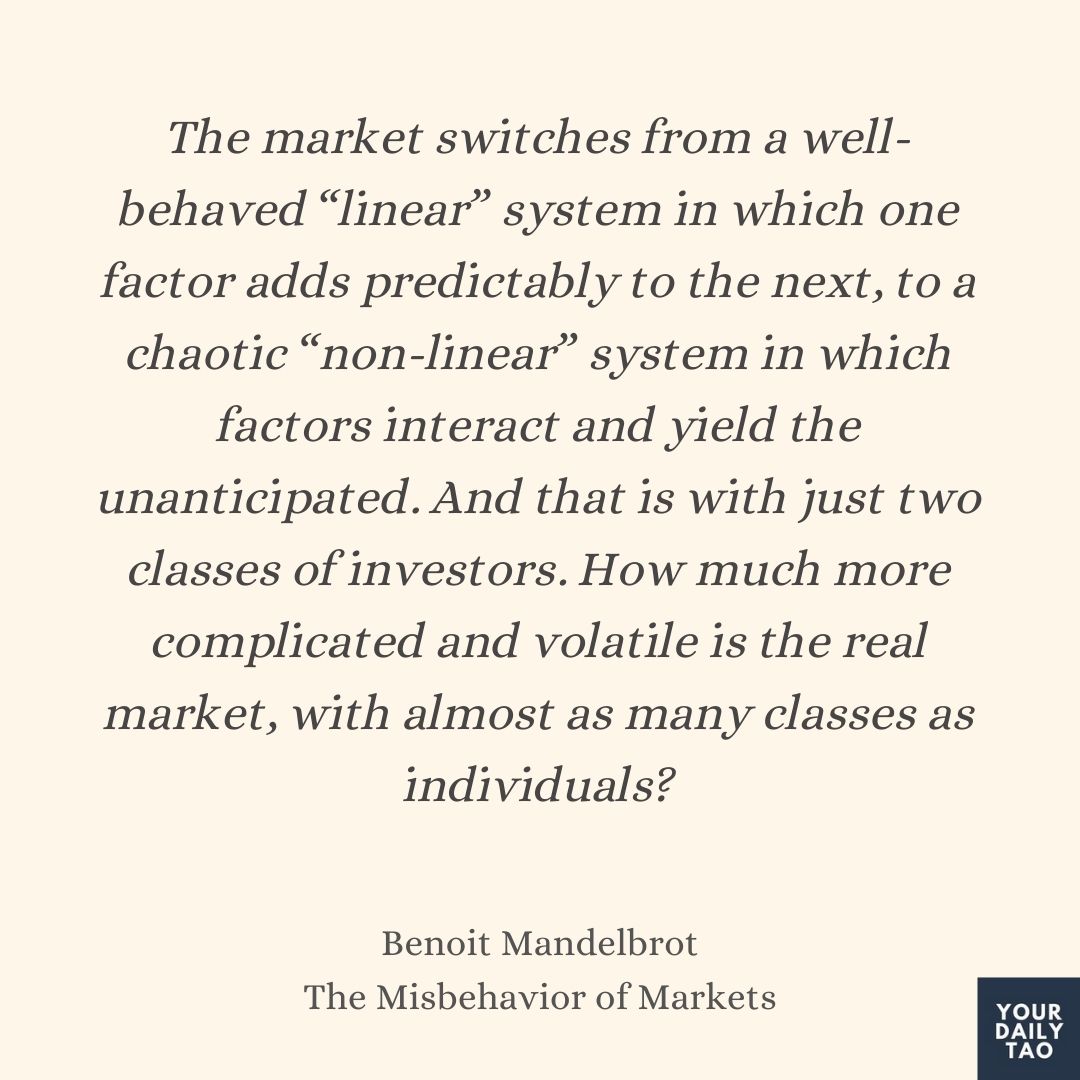

Once you drop the assumption of homogeneity, new and complicated things happen in your mathematical models of the market. For instance, assume just two types of investors, instead of one: fundamentalists who believe that each stock or currency has its own, intrinsic value and will eventually sell for that value, and chartists who ignore the fundamentals and only watch the price trends so they can jump on and off bandwagons. In computer simulations by economists Paul De Grauwe and Marianna Grimaldi at the Catholic University of Leuven, in Belgium, the two groups start interacting in unexpected ways, and price bubbles and crashes arise, spontaneously. The market switches from a well-behaved “linear” system in which one factor adds predictably to the next, to a chaotic “non-linear” system in which factors interact and yield the unanticipated. And that is with just two classes of investors. How much more complicated and volatile is the real market, with almost as many classes as individuals?

Understanding the intrinsic value of a company/business that is traded might not lend much help in predicting its stock price. In this passage, even simulations of 2 different classes of investors, 1 that focuses on fundamentals and 1 that focuses on pure technical (charts) can lead to unpredictable swings in the stock price as they impact each other.

What more in the today’s world, where not only do we have various classes of investors, but social movements and online communities (as is the case of GameStop and Reddit). As the number of actors influencing the prices of stocks increase, there is bound to be increased unpredictability of stocks.