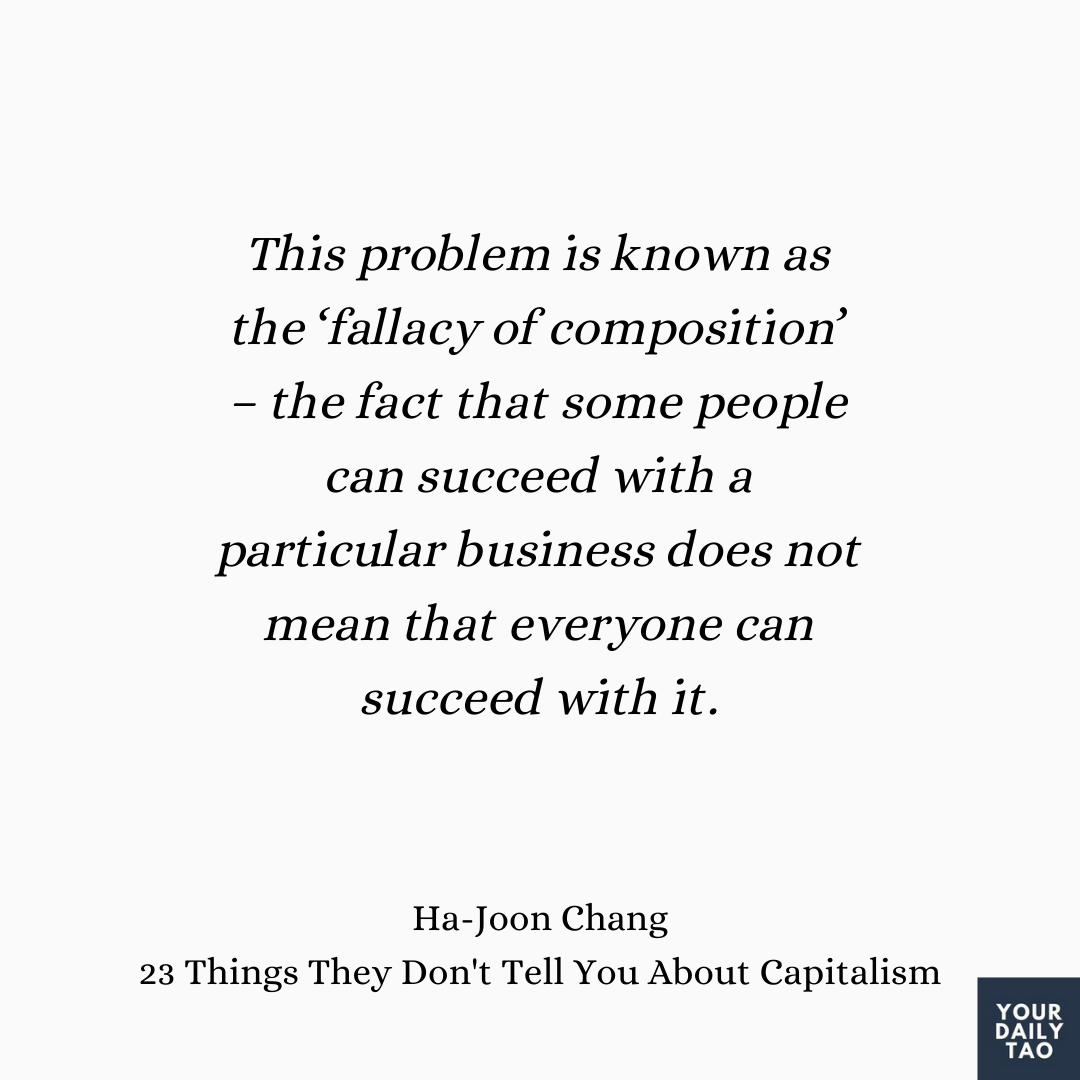

For example, when in 1997 the Grameen Bank teamed up with Telenor, the Norwegian phone company, and gave out microloans to women to buy a mobile phone and rent it out to their villagers, these ‘telephone ladies’ made handsome profits – $750–$1,200 in a country whose annual average per capita income was around $300. However, over time, the businesses financed by microcredit become crowded and their earnings fall. To go back to the Grameen phone case, by 2005 there were so many telephone ladies that their income was estimated to be around only $70 per year, even though the national average income had gone up to over $450. This problem is known as the ‘fallacy of composition’ – the fact that some people can succeed with a particular business does not mean that everyone can succeed with it.

I might be a sour prick, but I’m always skeptical over the effectiveness of “successful case studies” as shown in these micro-loans programs. What works for 1 person, might not work once it begins to scale within a community. In other excerpts from his book, Ha-Joon Chang mentions that most microloans are also taken to fuel consumption, rather than for the purpose of entrepreneurship.

While these consumption might be usually things that help immensely, e.g. illness, weddings, fixing a leaky roof etc. I still can’t get around how direct cash transfers isn’t just a more elegant and more effective solution towards helping the poor.